You may notice a significant difference in your credit score when you look at your credit reports. It doesn't always mean you are in financial distress, or that you're displaying bad behavior. However, there are a few reasons why your score could be a bit higher or lower than it should be. Most cases are due to errors or differences in reporting. You can fix any errors by working directly with the creditor or the credit bureau.

Credit reporting agencies can use a variety different scoring models. Each one weighs information differently. FICO is the most popular scoring model. VantageScore also has a scoring model, but requires more data.

A Consumer Financial Protection Bureau new study found that consumers may receive drastically different scores from their creditors. This is due to companies not reporting to all three of the main credit reporting agency (CRAs), in the United States. It's because CRAs use a variety of scoring models and rely heavily on different types financial data.

A Dodd-Frank Act study prompted the Consumer Financial Protection Bureau (CFPB) to do a variety of studies to examine the different credit scores and other similar functions. They were not designed to determine whether or otherwise credit rating agencies are trying to fool consumers through their scoring systems. However, the results were very interesting.

FICO is the most basic credit scoring method. This is the credit score that most people will see in their credit reports. This score generally shows your credit history, usage, as well as other information that lenders use to determine whether you're a risk. Creditors see the score as a measure to assess your risk of not repaying your debt. However, this score may vary from one bureau.

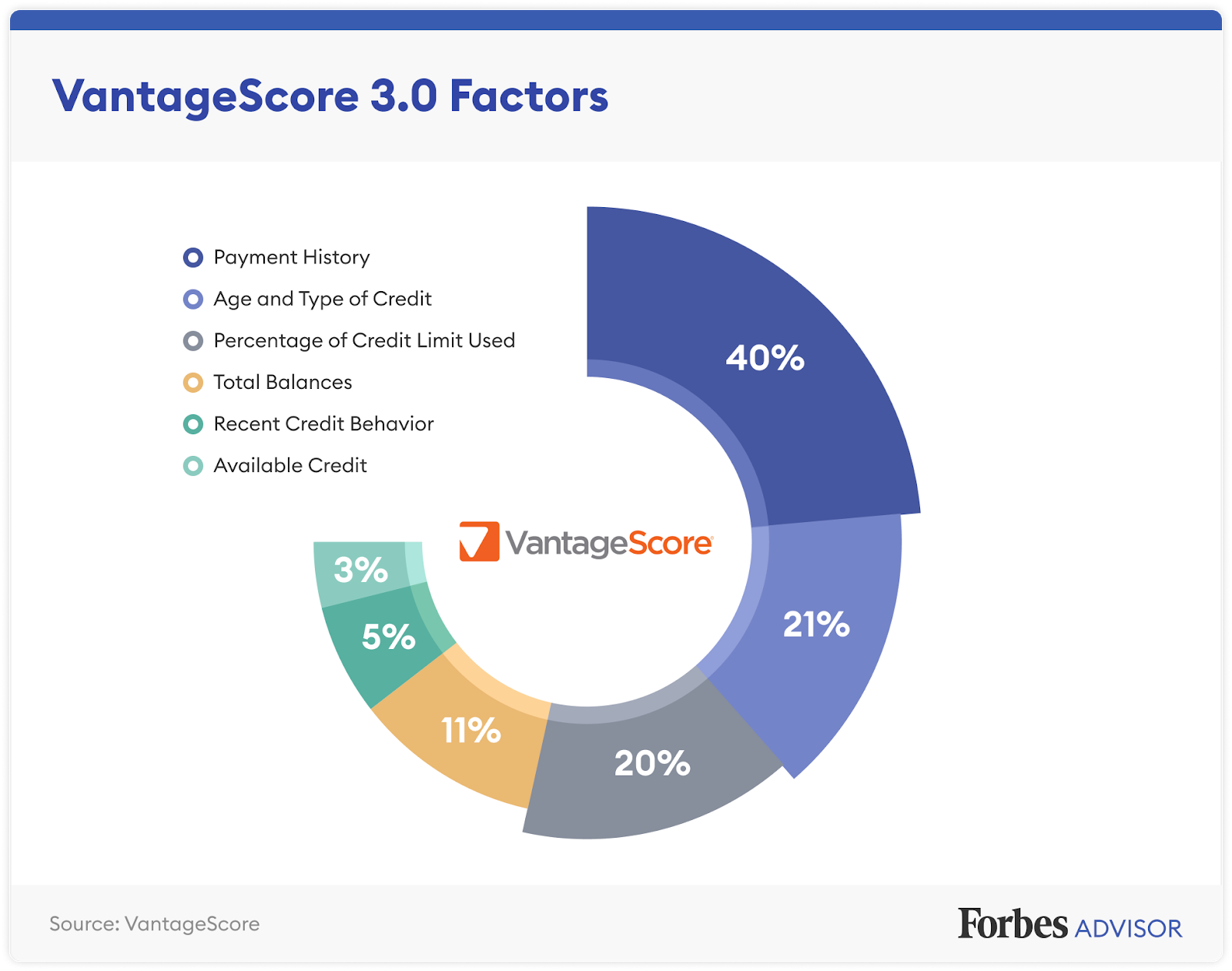

VantageScore is a similar scoring system. It focuses on the amount of your credit card and loan payments over time. To evaluate your credit history and weigh the amount of debt you have, the scoring model takes into account a variety of factors such as your credit history length, your recent payments, and your most recent credit card transactions.

One of the most interesting differences in credit scores is between rural and urban consumers. Although both have the same credit rating system, the average credit score for the former group is much lower. These scores may be affected by the local economy or population. Urban areas are generally more financially secure, and those living in metropolitan areas tend to have more favorable credit behaviors.

A consistent reporting pattern is one of the best ways to improve your score. Contact your creditor immediately if you are not able to get your credit limit reported to all three credit bureaus. You should be able for them to correct the error but it could take some time.

There are other factors that can affect your score, including a credit card account that is not reported to the credit bureaus. Check your credit report for any errors. This includes past names, loan amounts, credit cards, and your own name.